I am a PhD candidate in the Department of Finance at the University of Luxembourg.

My research applies advanced quantitative methods, including machine learning and econometric techniques, to two primary areas: macroeconomic analysis and digital asset pricing. This work combines empirical analysis with economic theory to investigate market dynamics, valuation mechanisms, and risk factors in both traditional and digital financial markets.

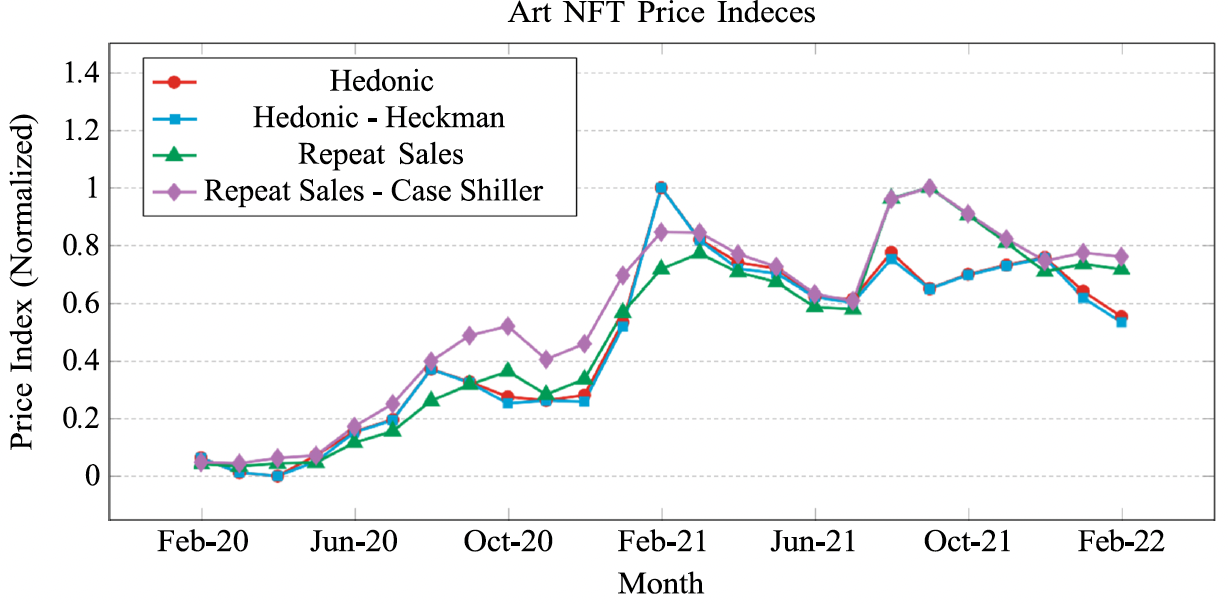

This paper analyzes the sales of 875,389 art nonfungible tokens (NFTs) on the Ethereum blockchain to identify the key determinants influencing NFT pricing and market dynamics. We find that market liquidity and trade volume are strong predictors of NFT prices. Contrarily, social media activity negatively correlates with prices. Introducing an artist ranking system, our study reveals a “superstar effect”, with a few artists dominating sales, and herding behaviour within the NFT market.

@article{fridgen2025pricing,title={Pricing dynamics and herding behaviour of NFTs},author={Fridgen, Gilbert and Kr{\"a}ussl, Roman and Papageorgiou, Orestis and Tugnetti, Alessandro},journal={European Financial Management},volume={31},number={2},pages={670--710},year={2025},doi={10.1111/eufm.12506},url={https://onlinelibrary.wiley.com/doi/full/10.1111/eufm.12506},dimensions={true},}